A huge challenge for U.S. workers over the past 20 years has been that we've been put in charge of managing our own retirement assets. Defined contribution plans via the 401k and its brethren have replaced defined benefit plans. This means we have been put on the front line of understanding the trade-off between risk and return, the principles of portfolio construction, and the art of rebalancing. And this has put us face-to-face with fund providers.

Fund providers for 401ks are broker/dealers. They are product sales people. With most 401ks, participants have no choice - they have to go with the fund provider. This can be very costly; but if the company has a match, this is still the way to go. In the process, Wall Street enriches itself on the backs of participants and companies - but that's a whole different story.

Over time, the process evolves for many of us . We change jobs, roll over 401ks, amass savings outside the company 401k, etc. This presents choices. We can continue the broker/dealer route, go with a registered investment advisor, or go it alone. Understanding the alternatives between broker dealers, i.e. non-fiduciaries and fee-only RIAs, i.e. fiduciaries is important and can be a critical factor in this decision.

Most of us first became acquainted with the broker/dealer in a company meeting held by the human resources department. He or she explained the plan, the matching features, and the investment choices. Typically it was a lot of jargon, it involved a lot of multi-colored charts, and if it lasted more than 30 minutes, it led to eyes glazing over and considerable nodding off.

The results of these meetings are disheartening when seen from my side of the table. I've seen too many portfolios of high commission, load funds, paying 12b-1 fees and excessive management fees that have eaten away at workers' nest eggs.

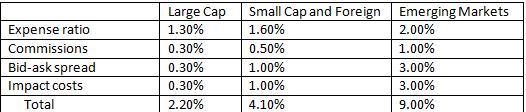

Fund Costs

As an aside, here is an estimate of average fund costs by William Bernstein from The Investor's Manifesto:

|

| Source: Bernstein, The Investor's Manifesto, p. 80 |

Fiduciaries vs. Non-Fiduciaries

These human resource meetings take place every day across the country, and many college graduates will soon attend them. The important fact to understand is that the presenters are not fiduciaries. This simply means that they do not necessarily have the participant's best interests at heart. Their allegiance is to their company and to their stock holders.

To see exactly how this works, ask some questions? To begin with, ask the plan rep how they are compensated. Ask them how it is that they offer funds outside of their family of funds. Ask them how and why these funds were chosen and how they get compensated when people choose these funds. Ask them why the introductory booklet they handed out, that describes the funds offered, doesn't have the expense ratio of the funds presented. In getting answers to these questions all I can say is "good luck."

Supposedly starting next year, fund providers will be dragged front and center and be required by law to fully disclose all costs. This is a huge step in the right direction because for the first time 401k participants will be able to understand exactly what their plan participation is costing. Don't be surprised if some of the big players announce fee cuts. This should tell you something.

In contrast, the fee-only registered investment advisor gets paid only by their clients. In other words, they don't sell products and, thereby, get paid commissions on what they sell. RIAs are fiduciaries. They are required to disclose all conflicts of interest. For example, if they refer you to an estate attorney from whom they get referrals, it has to be disclosed. Most important, a fee-only RIA has no incentive to put you in a high-priced fund. Indeed, if they are paid a percentage of the market value of your assets, they have a strong incentive to see that costs are minimized.

Disclosure: I am a fee-only registered investment advisor.

"Supposedly starting next year, fund providers will be dragged front and center and be required by law to fully disclose all costs. This is a huge step in the right direction "

ReplyDeleteAbsolutely! I don't know which senator was responsible for this, but hats off to him!

To me it's one of those no brainers. Similarly the Federal Government has arguably the best qualified plan in the country with its low fees and index choices. Why can't the rest of the country have the same? Why is everybody else enmeshed in this hidden fees fiasco for their retirement accounts?

ReplyDelete