A bit of back story: The younger daughter graduated from the Culinary Institute of America in New York as a pastry chef, worked for several months in Australia, spent time traveling in New Zealand and India, and now is taking her first "real" American job at a restaurant opening on the Eastern Shore in Maryland. She is 23 years old--soon to be 24.

Mom moves her into her new apartment. Pop gets the details on the 401k.

Keep in mind I've managed assets for 30 years as we try to look, from the perspective of a young pastry chef, at "Your Guide to Getting Started" put out by her fund provider Fidelity. Also keep in mind that Fidelity is one of the biggest players in the 401k market.

The booklet starts out with something us investment types (of which I guess I'm one) like: a bar graph showing the importance of saving and investing as soon as possible. It assumes a certain salary and shows her account balance at certain ages depending on the percent of salary contributed and a 7% return average annualized return. Great stuff. Not sure what the typical kitchen person or wait person will get out of it, but still all financial planner/investment types love this stuff.

Page 4 gets into eligibility, how to enroll (go to www.401k.com) and how to complete beneficiary form. It indicates when enrollment is effective, how much can be contributed, and how previous 401ks can be rolled into this one.

Next are two really important points: matching and vesting. Her plan matches 100% of the first 3% contributed and 50% of the next 3%. So, for example, if she makes $40,000/year, she will contribute $2,400 (.06*40,000). The company will chip in $1,200 for the first $1,200 and $600 for the next $1,200. The total contribution then would be $4,200 for the year, with $1,800 of that being "free money."

On the very next phone call, my pressing question is "Jill, can you put 6% of what you make

pre-tax into your 401k?"

Over the next 40 years, if the average annual return of the investment is 8%, that single contribution for her first year working will have grown to $91,243, (4,200* (1.08)^40) ! Her father's advice:

do what you have to do, but contribute the 6% of salary to take full advantage of the match.

Next, the booklet points out that, to be fully vested, you have to work for the restaurant for 2 years. Tack on advice:

plan on working 2 years.

OK...so far so good. Everybody's on the same page. The rest of page 5 in the booklet talks about taking a loan from the account (don't do it), withdrawals (forget about it), planning for retirement ( start reading it in 30 years). So basically, up to this point, she really didn't need me. In fact, very little of these first few pages needed to be read. The bottom line is participate up to the match. It is important not to get bogged down in minutiae because the brain numbing part is straight ahead - in other words, the whitewater is right around the bend.

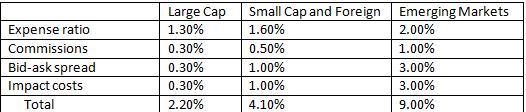

Page 8 starts with the investment nitty gritty. There we find an investment spectrum showing the list of investment choices in an horizontal framework ranging from most conservative ( money market) to more aggressive ( "Select Leisure Portfolio"). Here we get the line "For more complete information about any of the mutual funds available through the plan,

including fees and expenses, log on to ...". In fact, jumping ahead, there is nothing in the booklet as far as I could tell that specifies fees and expenses, although I can't swear to it because there is an awful lot of fine print.

Next we get into the fun part, and remember we are looking at this through the eyes of someone trained in the culinary arts. It makes us want to throw a recipe for creme brulee in front of the Fidelity reps and tell them to go make it and their future depends on how it turns out.

The Investment "Options"

There are 35 fund choices. There is the "Buffalo Small Cap Fund," the "Fidelity Contrafund," and Oakmark Equity and Income Fund Class I" fund. In fact, looking across all the funds, there are all kinds of classes including "investor class," administrative class," "class I," "class P," etc. There are indexed funds and enhanced indexed funds. There are even "hybrid funds" and a "Four-in-one Index Fund."

Tomorrow we'll move deeper into the abyss and think about appropriate investment choices for a budding pastry chef.