There are obviously different ways to do this. There is no absolute right way. What is important is that you do it, not so much how you do it. This is in the "there is more than one way to skin a cat" bucket. It is worth pointing out , however, that, by actually rebalancing on a regular basis, you will have an understanding of how your portfolio is positioned. DIY Investor appreciates that this is elementary to many readers, but he comes across plenty of investors who rebalance on an ad hoc basis. DIY Investor believes strongly that not knowing exactly how you are positioned and how performance is unfolding is a primary cause of the harmful emotional responses that occur in volatile markets.

Again, a systematic rebalancing plan presupposes that you have specific detail on portfolio positioning.

5% Rebalancing Rule

Investors use different ways and rules on how to rebalance, DIY Investor uses the 5% rule. If a portfolio class is more than 5% out of balance, then the portfolio has to be rebalanced. This is easy in today's world with the commission-free ETFs many brokers offer. Let's get down to specifics by using Schwab's tools. As always, DIY Investor urges all do-it-yourself investors to putter around on their broker's site to thoroughly understand the portfolio tools at their disposal. For our purpose, we'll use Schwab, the discount broker used by most of my clients.

Schwab offers 6 model portfolios, ranging from the most conservative with 0% stocks to the most aggressive with 95% stocks. Let's consider the popular "Moderate" portfolio which has 60% stocks and 40% fixed. This portfolio is used many times by investors moving into retirement.

|

| Source: Schwab |

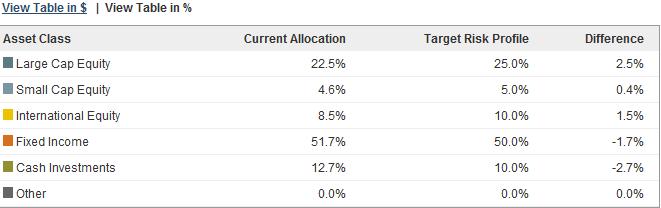

Again, consider a specific example:

|

| Source: Schwab |

Click to Enlarge Now look at the right-hand column. This column shows the difference, by asset class, between actual portfolio sector holdings and the targeted percentage. Whenever it gets 5% off target, DIY Investor rebalances.

Assume, for the sake of argument, that the international sector had performed poorly and was 5% under target. Typically, DIY Investor would handle this by buying shares of SCHF, Schwab's international ETF, for a zero commission and an expense ratio of .13%.

DIY Investor wants to emphasize how important it is to grasp the ease with which this is all done. Check this allocation once a month, and you'll be fine. Whenever the market makes a big move, check to be sure exactly where you stand.

As an added guidepost check performance:

| Source: Schwab |

Disclosure: The information presented here is for educational purposes only. No specific securities are recommended. Investors should do their own research and consult with a professional before making investments. I am not affiliated with Charles Schwab and receive no compensation from them.

Robert, good educational article, much appreciated.

ReplyDeleteI prefer to rebalance rather than try to guess where the tops and bottoms are. I find it's easier to deal with emotionally and I think it works better this way, too.

ReplyDelete@The Grouch Thanks.

ReplyDelete@Invest It Wisely Actually rebalancing is a subtle way of buying low and selling high. Over time it actually adds to performance. Furthermore if you want to market time at the margin you can move a few percent around here and there. I have to admit I structured the bond portion shorter than the overall bond market because rates were so low. It was an unusual situation. That's why the performance in the above table is a bit more than the benchmark. Actually over time the performance should be about 15 - 20 basis points below the benchmark because of the ETF management fees.

I too prefer the 5% rule when it comes to re-balancing!

ReplyDeleteSome prefer doing it once a year, that works too!

@MoneyCone As I say "there's more than one way to skin a cat" in a lot of this. I'll admit that sometimes after a big down day I'll push up the amount in the sector that dropped. 5% is bottom line, no thinking, automatic for me.

ReplyDeleteWhat are the tax implications of rebalancing?

ReplyDeleteDo you pay tax on the gains and get credit for the losers?